Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

6th Edition

ISBN: 9780134486857

Author: Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura

Publisher: PEARSON

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 24, Problem 24BP

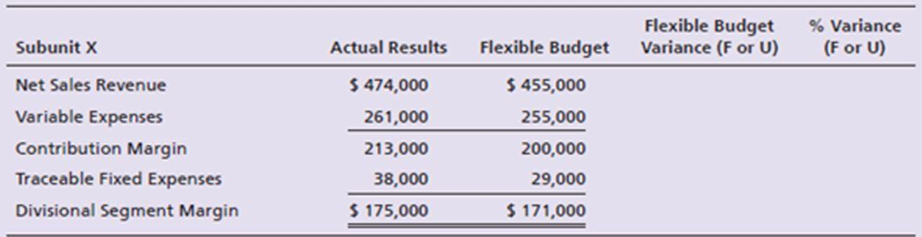

One subunit of Track Sports Company had the following financial results last month:

Requirements

- 1. Complete the performance evaluation report for this subunit (round to two decimal places).

- 2. Based on the data presented and your knowledge of the company, what type of responsibility center is this subunit?

- 3. Which items should be investigated if part of management’s decision criteria is to investigate all variances equal to or exceeding $8,000 and exceeding 10% (both criteria must be met)?

- 4. Should only unfavorable variances be investigated? Explain.

- 5. Is it possible that the variances are due to a higher-than-expected sales volume? Explain.

- 6. Will management place equal weight on each of the variances exceeding $8,000? Explain.

- 7. Which balanced scorecard perspective is being addressed through this performance report? In your opinion, is this performance report a lead or a lag indicator? Explain.

- 8. List one key performance indicator for the three other balanced scorecard perspectives. Make sure to indicate which perspective is being addressed by the indicators you list.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 24 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Ch. 24 - Prob. 1TICh. 24 - Fill in the blanks with the phrase that best...Ch. 24 - Prob. 3TICh. 24 - Fill in the blanks with the phrase that best...Ch. 24 - Prob. 5TICh. 24 - Fill in the blanks with the phrase that best...Ch. 24 - Prob. 7TICh. 24 - Prob. 8TICh. 24 - Prob. 9TICh. 24 - Prob. 10TI

Ch. 24 - Prob. 11TICh. 24 - Prob. 12TICh. 24 - Prob. 13TICh. 24 - Match the responsibility center to the correct...Ch. 24 - Prob. 15TICh. 24 - Prob. 16TICh. 24 - Prob. 17TICh. 24 - Prob. 18TICh. 24 - Prob. 19TICh. 24 - Prob. 20TICh. 24 - Sheffield Company manufactures power tools. The...Ch. 24 - Prob. 22TICh. 24 - Which is not one of the potential advantages of...Ch. 24 - The Quaker Foods division of PepsiCo is most...Ch. 24 - Which of the following is not a goal of...Ch. 24 - Which of the following balanced scorecard...Ch. 24 - The performance evaluation of a cost center is...Ch. 24 - Assume the Residential Division of Kipper Faucets...Ch. 24 - Assume the Residential Division of Kipper Faucets...Ch. 24 - Assume the Residential Division of Kipper Faucets...Ch. 24 - Assume the Residential Division of Kipper Faucets...Ch. 24 - Penn Company has a division that manufactures a...Ch. 24 - Explain the difference between a centralized...Ch. 24 - Prob. 2RQCh. 24 - List the disadvantages of decentralization.Ch. 24 - What is goal congruence?Ch. 24 - Prob. 5RQCh. 24 - What is the purpose of a responsibility accounting...Ch. 24 - Prob. 7RQCh. 24 - Prob. 8RQCh. 24 - Prob. 9RQCh. 24 - What are the goals of a performance evaluation...Ch. 24 - Prob. 11RQCh. 24 - How is the use of a balanced scorecard as a...Ch. 24 - What is a key performance indicator?Ch. 24 - What are the four perspectives of the balanced...Ch. 24 - Explain the difference between a controllable and...Ch. 24 - Prob. 16RQCh. 24 - What are two key performance indicators used to...Ch. 24 - Prob. 18RQCh. 24 - Prob. 19RQCh. 24 - Prob. 20RQCh. 24 - Prob. 21RQCh. 24 - Prob. 22RQCh. 24 - What is the biggest advantage of using RI to...Ch. 24 - What are some limitations of financial performance...Ch. 24 - Prob. 25RQCh. 24 - Prob. 26RQCh. 24 - Prob. 27RQCh. 24 - Prob. 1SECh. 24 - Prob. 2SECh. 24 - Well-designed performance evaluation systems...Ch. 24 - Consider the following key performance indicators,...Ch. 24 - Management by exception is a term often used in...Ch. 24 - Consider the following data, and determine which...Ch. 24 - XTreme Sports Company makes snowboards, downhill...Ch. 24 - Prob. 8SECh. 24 - Using ROI and RI to evaluate investment centers...Ch. 24 - Henderson Company manufactures electronics. The...Ch. 24 - Prob. 11ECh. 24 - Prob. 12ECh. 24 - Well-designed performance evaluation systems...Ch. 24 - Consider the following key performance indicators,...Ch. 24 - One subunit of Harris Sports Company had the...Ch. 24 - The accountant for a subunit of Speed Sports...Ch. 24 - Zims, a national manufacturer of lawn-mowing and...Ch. 24 - Refer to the data in Exercise E24-17. Calculate...Ch. 24 - Prob. 19ECh. 24 - One subunit of Racer Sports Company had the...Ch. 24 - Consider the following condensed financial...Ch. 24 - Prob. 22APCh. 24 - The Harris Company is decentralized, and divisions...Ch. 24 - One subunit of Track Sports Company had the...Ch. 24 - Consider the following condensed financial...Ch. 24 - Prob. 26BPCh. 24 - The Hernandez Company is decentralized, and...Ch. 24 - Prob. 28PCh. 24 - This problem continues the Piedmont Computer...Ch. 24 - The Trolley Toy Company manufactures toy building...Ch. 24 - Dixie Irwin is the department manager for...Ch. 24 - Prob. 1FCCh. 24 - In 150 words or fewer, list each of the four...

Additional Business Textbook Solutions

Find more solutions based on key concepts

(a) Standard costs are the expected total cost of completing a job. Is this correct? Explain, (b) A standard im...

Managerial Accounting: Tools for Business Decision Making

18. What is the calculation for return on assets (ROA)? Explain what ROA measures.

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Place the letter of the appropriate accounting cost in Column 2 in the blank next to each decision category in ...

Fundamentals of Cost Accounting

Preparing Financial Statements from a Trial Balance The following accounts are taken from Equilibrium Riding, I...

Fundamentals of Financial Accounting

Fundamental and Enhancing Characteristics. Identify whether the following items are fundamental characteristics...

Intermediate Accounting

1. For Frank’s Funky Sounds, straight-line depreciation on the trucks is a

Learning Objective 1

a. variable cos...

Horngren's Accounting (12th Edition)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Uchdorf Manufacturing just completed a study of its purchasing activity with the objective of improving its efficiency. The driver for the activity is number of purchase orders. The following data pertain to the activity for the most recent year: Activity supply: five purchasing agents capable of processing 2,400 orders per year (12,000 orders) Purchasing agent cost (salary): 45,600 per year Actual usage: 10,600 orders per year Value-added quantity: 7,000 orders per year Required: 1. Calculate the volume variance and explain its significance. 2. Calculate the unused capacity variance and explain its use. 3. What if the actual usage drops to 9,000 orders? What effect will this have on capacity management? What will be the level of spending reduction if the value-added standard is met?arrow_forwardCassara, Inc., had the following quality costs for the years ended December 31, 20X1 and 20X2: At the end of 20X1, management decided to increase its investment in control costs by 40% for each categorys items, with the expectation that failure costs would decrease by 25% for each item of the failure categories. Sales were 12,000,000 for both 20X1 and 20X2. Required: 1. Calculate the budgeted costs for 20X2, and prepare an interim quality performance report. 2. Comment on the significance of the report. How much progress has Cassara made?arrow_forwardKavallia Company set a standard cost for one item at 328,000; allowable deviation is 14,500. Actual costs for the past six months are as follows: Required: 1. Calculate the variance from standard for each month. Which months should be investigated? 2. What if the company uses a two-part rule for investigating variances? The allowable deviation is the lesser of 4 percent of the standard amount or 14,500. Now which months should be investigated?arrow_forward

- The normal capacity of a manufacturing plant is 30,000 direct labor hours or 20,000 units per month. Standard fixed costs are 6,000, and variable costs are 12,000. Data for two months follow: For each month, make a single journal entry to charge overhead to Work in Process, to close Factory Overhead, and to record variances. Indicate the types of variances and state whether each is favorable or unfavorable. (Hint: You must first compute the flexible-budget and production-volume variances.)arrow_forwardThe management of Golding Company has determined that the cost to investigate a variance produced by its standard cost system ranges from 2,000 to 3,000. If a problem is discovered, the average benefit from taking corrective action usually outweighs the cost of investigation. Past experience from the investigation of variances has revealed that corrective action is rarely needed for deviations within 8% of the standard cost. Golding produces a single product, which has the following standards for materials and labor: Actual production for the past 3 months follows, with the associated actual usage and costs for materials and labor. There were no beginning or ending raw materials inventories. Required: 1. What upper and lower control limits would you use for materials variances? For labor variances? 2. Compute the materials and labor variances for April, May, and June. Identify those that would require investigation by comparing each variance to the amount of the limit computed in Requirement 1. Compute the actual percentage deviation from standard. Round all unit costs to four decimal places. Round variances to the nearest dollar. Round variance rates to three decimal places so that percentages will show to one decimal place. 3. CONCEPTUAL CONNECTION Let the horizontal axis be time and the vertical axis be variances measured as a percentage deviation from standard. Draw horizontal lines that identify upper and lower control limits. Plot the labor and material variances for April, May, and June. Prepare a separate graph for each type of variance. Explain how you would use these graphs (called control charts) to assist your analysis of variances.arrow_forwardBudgeted unit sales for the entire countertop oven industry were 2,500,000 (of all model types), and actual unit sales for the industry were 2,550,000. Recall from Cornerstone Exercise 18.6 that Iliff, Inc., provided the following information: Required: 1. Calculate the market share variance (take percentages out to four significant digits). 2. Calculate the market size variance. 3. What if Iliff actually sold a total of 41,000 units (in total of the two models)? How would that affect the market share variance? The market size variance?arrow_forward

- Buenolorl Company produces a well-known cologne. The standard manufacturing cost of the cologne is described by the following standard cost sheet: Management has decided to investigate only those variances that exceed the lesser of 10% of the standard cost for each category or 20,000. During the past quarter, 250,000 four-ounce bottles of cologne were produced. Descriptions of actual activity for the quarter follow: a. A total of 1.35 million ounces of liquids was purchased, mixed, and processed. Evaporation was higher than expected. (No inventories of liquids are maintained.) The price paid per ounce averaged 0.42. b. Exactly 250,000 bottles were used. The price paid for each bottle was 0.048. c. Direct labor hours totaled 48,250, with a total cost of 733,000. Normal production volume for Buenolorl is 250,000 bottles per quarter. The standard overhead rates are computed by using normal volume. All overhead costs are incurred uniformly throughout the year. (Note: Round unit costs to the nearest cent and total amounts to the nearest dollar.) Required: 1. Calculate the upper and lower control limits for materials and labor. 2. Compute the total materials variance, and break it into price and usage variances. Would these variances be investigated? 3. Compute the total labor variance, and break it into rate and efficiency variances. Would these variances be investigated?arrow_forwardThe controller of Emery, Inc. has computed quality costs as a percentage of sales for the past 5 years (20X1 was the first year the company implemented a quality improvement program). This information is as follows: Required: 1. Prepare a trend graph for total quality costs. Comment on what the graph has to say about the success of the quality improvement program. 2. Prepare a graph that shows the trend for each quality cost category. What does the graph have to say about the success of the quality improvement program? Does this graph supply more insight than the total cost trend graph does? 3. Prepare a graph that compares the trend in relative control costs versus relative failure costs. Comment on the significance of this trend.arrow_forwardNabors Company had actual quality costs for the year ended June 30, 20x5, as given below. At the zero-defect state, Nabors expects to spend 375,000 on quality engineering, 75,000 on vendor certification, and 50,000 on packaging inspection. Assume sales to be 25,000,000. Required: 1. Prepare a long-range performance report for 20x5. What does this report tell the management of Nabors? 2. Explain why quality costs still are present for the zero-defect state. 3. What if Nabors achieves the zero-defect state reflected in the report? What are some of the implications of this achievement?arrow_forward

- Javier Company has sales of 8 million and quality costs of 1,600,000. The company is embarking on a major quality improvement program. During the next three years, Javier intends to attack failure costs by increasing its appraisal and prevention costs. The right prevention activities will be selected, and appraisal costs will be reduced according to the results achieved. For the coming year, management is considering six specific activities: quality training, process control, product inspection, supplier evaluation, prototype testing, and redesign of two major products. To encourage managers to focus on reducing non-value-added quality costs and select the right activities, a bonus pool is established relating to reduction of quality costs. The bonus pool is equal to 10 percent of the total reduction in quality costs. Current quality costs and the costs of these six activities are given in the following table. Each activity is added sequentially so that its effect on the cost categories can be assessed. For example, after quality training is added, the control costs increase to 320,000, and the failure costs drop to 1,040,000. Even though the activities are presented sequentially, they are totally independent of each other. Thus, only beneficial activities need be selected. Required: 1. Identify the control activities that should be implemented, and calculate the total quality costs associated with this selection. Assume that an activity is selected only if it increases the bonus pool. 2. Given the activities selected in Requirement 1, calculate the following: a. The reduction in total quality costs b. The percentage distribution for control and failure costs c. The amount for this years bonus pool 3. Suppose that a quality engineer complained about the gainsharing incentive system. Basically, he argued that the bonus should be based only on reductions of failure and appraisal costs. In this way, investment in prevention activities would be encouraged, and eventually, failure and appraisal costs would be eliminated. After eliminating the non-value-added costs, focus could then be placed on the level of prevention costs. If this approach were adopted, what activities would be selected? Do you agree or disagree with this approach? Explain.arrow_forwardAt the end of 20x1, Mejorar Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To lower costs, Mejorar undertook a number of improvement activities such as JIT production, total quality management, and activity-based management. Now, after two years of operation, the president of Mejorar wants some assessment of the achievements. To help provide this assessment, the following information on one product has been gathered: Required: 1. Compute the following measures for 20x1 and 20x3: a. Actual velocity and cycle time b. Percentage of total revenue from new customers (assume one unit per customer) c. Percentage of very satisfied customers (assume each customer purchases one unit) d. Market share e. Percentage change in actual product cost (for 20x3 only) f. Percentage change in days of inventory (for 20x3 only) g. Defective units as a percentage of total units produced h. Total hours of training i. Suggestions per production worker j. Total revenue k. Number of new customers 2. For the measures listed in Requirement 1, list likely strategic objectives, classified according to the four Balance Scorecard perspectives. Assume there is one measure per objective.arrow_forwardCortez Manufacturing, Inc. has the following flexible budget formulas and amounts: Actual results for May for the production and sale of 5,000 units were as follows: Prepare a performance report for May that includes the identification of the favorable and unfavorable variances.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Responsibility Accounting| Responsibility Centers and Segments| US CMA Part 1| US CMA course; Master Budget and Responsibility Accounting-Intro to Managerial Accounting- Su. 2013-Prof. Gershberg; Author: Mera Skill; Rutgers Accounting Web;https://www.youtube.com/watch?v=SYQ4u1BP24g;License: Standard YouTube License, CC-BY