Videos

Using High-Low to Calculate Fixed Cost, Calculate the Variable Rate, and Construct a Cost Function

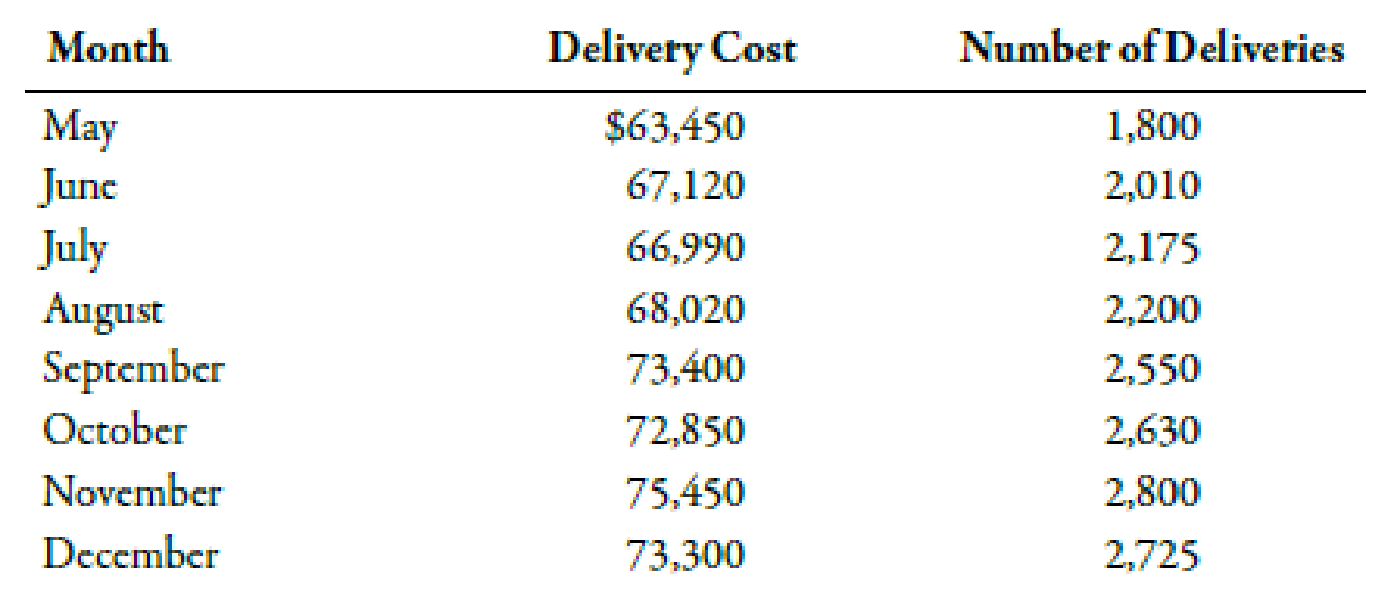

Refer to the information for Speedy Pete’s above. Speedy Pete’s controller wants to calculate the fixed and variable costs associated with its cutting-edge delivery service.

Required:

Using the high-low method, calculate the fixed cost of deliveries, calculate the variable rate per delivery, and construct the cost formula for total delivery cost.

Use the following information for Brief Exercises 3-26 through 3-29:

Speedy Pete’s is a small start-up company that delivers high-end coffee drinks to large metropolitan office buildings via a cutting-edge motorized coffee cart to compete with other premium coffee shops. Data for the past 8 months were collected as follows:

Trending nowThis is a popular solution!

Chapter 3 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- The management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardContinuous improvement is the governing principle of a lean accounting system. Following are several performance measures. Some of these measures would be associated with a traditional standard-costing accounting system, and some would be associated with a lean accounting system. a. Materials price variances b. Cycle time c. Comparison of actual product costs with target costs d. Materials quantity or efficiency variances e. Comparison of actual product costs over time (trend reports) f. Comparison of actual overhead costs, item by item, with the corresponding budgeted costs g. Comparison of product costs with competitors product costs h. Percentage of on-time deliveries i. First-time through j. Reports of value- and non-value-added costs k. Labor efficiency variances l. Days of inventory m. Downtime n. Manufacturing cycle efficiency (MCE) o. Unused (available) capacity variance p. Labor rate variance q. Using a sister plants best practices as a performance standard Required: 1. Classify each measure as lean or traditional (standard costing). If traditional, discuss the measures limitations for a lean environment. If it is a lean measure, describe how the measure supports the objectives of lean manufacturing. 2. Classify the measures into operational (nonfinancial) and financial categories. Explain why operational measures are better for control at the shop level (production floor) than financial measures. Should any financial measures be used at the operational level? 3. Suggest some additional measures that you would like to see added to the list that would be supportive of lean objectives.arrow_forwardVariable and Fixed Costs, Cost Formula, High-Low Method Li Ming Yuan and Tiffany Shaden are the department heads for the accounting department and human resources department, respectively, at a large textile firm in the southern United States. They have just returned from an executive meeting at which the necessity of cutting costs and gaining efficiency has been stressed. After talking with Tiffany and some of her staff members, as well as his own staff members, Li Ming discovered that there were a number of costs associated with the claims processing activity. These costs included the salaries of the two paralegals who worked full time on claims processing, the salary of the accountant who cut the checks, the cost of claims forms, checks, envelopes, and postage, and depreciation on the office equipment dedicated to the processing. Some of the paralegals time appears to vary with the routine processing of uncontested claims, but considerable time also appears to be spent on the claims that have incomplete documentation or are contested. The accountants time appears to vary with the number of claims processed. Li Ming was able to separate the costs of processing claims from the costs of running the departments of accounting and human resources. He gathered the data on claims processing cost and the number of claims processed per month for the past 6 months. These data are as follows: Required: 1. Classify the claims processing costs that Li Ming identified as variable and fixed. 2. What is the independent variable? The dependent variable? 3. Use the high-low method to find the fixed cost per month and the variable rate. What is the cost formula? 4. CONCEPTUAL CONNECTION Suppose that an outside company bids on the claims processing business. The bid price is 4.60 per claim. If Tiffany expects 75,600 claims next year, should she outsource the claims processing or continue to do it in-house?arrow_forward

- The graphs below represent cost behavior patterns that might occur in acompany's cost structure. The vertical axis represents total cost, and thehorizontal axis represents activity output. Required:For each of the following situations, choose the graph from the group a-1 that best illustrates the cost pattern involved. Also, for each situation,identify the driver that measures activity output. 1. The cost of power when a fixed fee of $500 per month is chargedplus an additional charge of $0.12 per kilowatt-hour used2. Commissions paid to sales representatives. Commissions arepaid at the rate of 5 percent of sales made up to total annual salesof $500,000, and 7 percent of sales above $500,000.3. A part purchased from an outside supplier costs $12 per part for the first 3,000 parts and $10 per part for all parts purchased inexcess of 3,000 units.4. The cost of surgical gloves, which are purchased in incrementsof 100 units (gloves come in boxes of 100 pairs).5. The cost of tuition at a…arrow_forwardThe MTN Company has assembled the following data pertaining to certain costs which cannot be easily identified as either fixed or variable. MTN has heard about a method of measuring cost functions called the high-low method and has decided to use it in this situation Cost Hours $100,000 3,500 61,o00 2,000 85,000 2,600 78,200 2,450 91,000 3,000 110,400 3,900 106,000 3,740 93,000 3,380 Calculate the variable cost per hour Calculate the total fixed costs Write the equation which measures the cost behavior of the costs Calculate the operating costs for 3,750arrow_forwardEmployee training is an example of discretionary fixed costs. Select one: True False Below are the measures of cost functions except: a. Regression analysis b. Engineering analysis c. Visual fit analysis d. Maintenance analysis Cost behavior is linear in nature on cost driver levels. Select one: True False Discretionary cost are the fixed cost that are able to achieve at desired level of service or production. Select one: True False Period costs are the cost identified with goods produced. Select one: True False Lease payment is the example of discretionary fixed cost. Select one: True False Below are the examples of committed costs, except: a. Mortgage payment b. Depreciation c. Tax payment d. Management salary Direct labor cost includes wages of all the labors that can be traced specifically. Select one: True False Cost are assumed to be fixed or changes within the relevant range of activity. Select one: True Falsearrow_forward

- The MTN Company has assembled the following data pertaining to certain costs which cannot be easily identified as either fixed or variable. MTN has heard about a method of measuring cost functions called the high-low method and has decided to use it in this situation. Cost Hours $100,000 3,500 61,000 2,000 85,000 2,600 78,200 2,450 91,000 3,000 110,400 3,900 106,000 3,740 93,000 3,380 a) Calculate the variable cost per hour b) Calculate the total fixed costs c) Write the equation which measures the cost behavior of the costs d) Calculate the operating costs for 3,750 hours.arrow_forward1.The relevant costing involves making decision to the following, except: Select one: a. overcome limited factors. b. price higher or lower. c. accept or reject a special order. d. keep or drop a segment or product line. 2.Below are the methods to compute the break-even point, except: Select one: a. contribution margin method. b. cost-volume-profit graphic presentation. c. mathematical equation method. d. profit margin method. 3.The financial budget comprises of the following, except: Select one: a. cash budget. b. investment budget. c. budgeted cash flows. d. capital budget.arrow_forwarda) Determine the variable cost per unit and the fixed cost using the high-low method.b) What is the equation of the total mixed cost function?c) Prepare the scatter diagram and insert the trendline or line of best-fit. Use a scaleof 2 cm to represent 1,000 units on the x-axis & 2 cm to represent $50,000 on the yaxis.arrow_forward

- 1. One way management considers their costs is as average costs. Under this approach, managers can calculate both average fixed and average variable costs. Average fixed cost (AFC) is the total fixed costs divided by the total number of units produced, which results in a per-unit cost. Average variable cost (AVC) is the total variable costs divided by the total number of units produced, which results in a per-unit cost. Management knows that long as the price they receive for their products is greater than the per-unit AVC, they are not only covering the variable cost of production, but each boat is making a contribution toward covering fixed costs. True / False 2. Product costs are all those associated with the acquisition or production of goods and products. When products are purchased for resale, the cost of goods is recorded as an asset on the company’s balance sheet. It is not until the products are sold that they become an expense on the income statement. By moving product…arrow_forwardWhen faced with a limited availability of machine-hours,management should consider producing those products that:a. Have the highest contribution margin per unit.b. Have the highest contribution margin ratios.c. Require the fewest machine-hours to produce.d. Contribute the highest contribution margin permachine-hour.arrow_forwardContribution Margin, Cost-Volume-Profit Analysis and Break-Even Point (Overview) Fixed, Variable and Mixed Costs An appreciation of cost behavior is needed in order for management to understand and predict profitability as the costs of material, labor and other operating expenses and levels of production and sales change. It's important to review the cost behavior of fixed, variable and mixed costs before contribution margins, cost-volume-profit analysis, and break-even points. 1. In the table below, Have-A-Seat Inc. has outlined many of the costs associated with producing office chairs. With respect to the production and sale of office chairs, classify each cost as fixed, mixed, or variable. a. Pressure-molded plastic for chair frames b. Pension cost: $0.50 per employee hour on the job c. Insurance premiums for inventory: $2,100 per month plus $0.01 for each dollar of inventory over $2 million d. Property taxes: $120,000 per year for the factory building and…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning